If you own a unit, factory or commercial lot in a body corporate or strata scheme, chances are you’ve asked this exact question:

“Do I need insurance for a strata property or does the body corporate insurance already cover me?”

It’s a fair question.

And it’s one that costs property owners tens of thousands of dollars every year when they assume the wrong answer. Because here’s the truth most people only learn after something goes wrong:

Body corporate insurance is essential but it is not complete protection for you as an owner.

We’re going to walk you through exactly what strata insurance covers, what they usually don’t, where the dangerous grey areas live and why relying on assumptions is one of the biggest risks in property ownership.

This isn’t theory.

This is based on real claims, real disputes and real money lost.

The Biggest Myth in Strata Property Insurance

“The body corporate covers everything.”

It doesn’t.

Body corporate (strata) insurance is designed to protect common property and shared assets – not your personal financial exposure as a property owner. That distinction is where most problems begin.

What is Body Corporate (Strata) Insurance?

In Australia, strata schemes are legally required to hold insurance under legislation such as legally required to hold insurance under legislation such as the Body Corporate and Community Management Act (QLD) and equivalent Acts in other states.

At a high level, body corporate insurance generally covers:

- The building structure

- Common property

- Certain shared services

- Public Liability in common areas

That sounds comprehensive… until you look closer.

What Body Corporate Insurance Usually Covers

Across most strata policies, cover typically includes:

Building structure and common property

- External walls

- Roof

- Shared stairwells

- Driveways

- Shared walls between lots

Public Liability (Common Areas)

- Injury or property damage to third parties in shared spaces

- Minimum $10-20 million cover (varies by state)

Machinery Breakdown (Common Assets)

- Lifts

- Shared air-conditioning

- Pumps and shared plant

What Body Corporate Insurance Usually Does Not Cover (And This Is Where Owners Get Burned)

Here’s where the risk lives.

Body corporate insurance does not automatically cover:

Inside Your Lot

- Internal carpets and flooring

- Blinds and curtains

- Built-in cupboards

- Internal fit-out

In-Unit Machinery and Fixtures

- Air-conditioning units servicing only your lot

- Hot water systems

- Fixed plant inside your unit

Public Liability Inside Your Unit

If someone is injured inside your lot and the tenant’s insurance doesn’t respond, wasn’t in place or there was a fitout works you were unaware of from the previous tenant, you as the owner can be held liable.

Slip. Trip. Injury. Claim.

That exposure sites squarely with you.

Tenant-Related Risks

- Malicious damage

- Negligent damage

- Accidental damage beyond the bond

- Tenant default and abandonment

Loss of Rent (In Many Scenarios)

Body corporate insurance may only cover loss of rent if the damage is caused by an insured event to common property.

If the loss is due to:

- Tenant default

- Vacancies during repairs

- Internal damage not covered by strata

You wear the cost.

So, do you need Insurance for Strata Property?

Most likely and you should definitely have a broker review the strata documents and tenants insurance/lease to identify any gaps. And not just “some” insurance. If you own a strata property, you typically need additional insurance on top of body corporate cover, such as:

Landlord Insurance (If the Property Is Leased)

Covers:

- Loss of rent due to tenant default (not all insurers cover this)

- Malicious or accidental tenant damage

- Legal expenses

- Liability gaps inside the lot

Contents Insurance (Even for Landlords)

Covers:

- Internal fixtures not insured by strata

- Owner-supplied items

- Flooring, blinds, fittings

Owner Public Liability (Inside the Lot)

Protects you if a tenant or visitor is injured inside your lot and the tenant’s policy has gaps.

The Grey Zones That Cause the Most Disputes

This is where we see owners get caught out the most.

Tenant-Installed Fixtures

Air-conditioning units, solar, stairwells, mezzanines often installed after the original lease.

If these are:

- Installed in common areas

- Approved under separate agreements

- Not disclosed to insurers

- Done with a previous owner and there’s now a new tenant and you’re unaware

They can fall outside both strata and landlord cover.

A Real-World Scenario (This Happens More Than You Think)

An owner assumed: “Body corporate insurance has it covered.”

A tenant defaulted and disappeared.

A separate agreement required a tenant-installed stairwell in a common area to be removed at make good and the document was not disclosed to the new property manager or the insurer.

Result?

- Tens of thousands in removal costs

- No Insurance coverage

- Owner paid out of pocket over $19,000

When the insurance broker was later asked if it could have been covered?

Yes. If it had been structured and disclosedcorrectly.

This is why insurance isn’t just about having a policy. It’s about understanding responsibility.

What You Should Do As A Strata Property Owner (Step-by-Step)

- Do not assume strata = full cover

- Review your Lease, By-Laws and any side agreements

- Confirm what’s inside vs outside your lot

- What fixtures belong to whom

- Speak with a licensed insurance broker (if they give you advice without reviewing documentation, get another opinion)

- Ensure policies align with your lease obligations, your risk exposure and your tenant profile.

Why This Matters More in Commercial Strata

Commercial strata properties amplify risk because:

- Fit-outs are more complex

- Leases shift responsibility

- Claims are larger

- Downtime costs more

This is where professional property management and insurance literacy separate protected owners from exposed ones.

So Your Original Question was “Do I Need Insurance for a Strata Property?”

Yes. Body Corporate insurance alone is usually not enough.

If you rely solely on strata cover, you are exposed to:

- In-unit liability

- Tenant damage

- Loss of rent

- Uninsured fixtures

- Costly grey-area disputes

Understanding where strata insurance stops – and owner responsibility begins – is one of the most important skills a property owner can have. And it’s why informed owners don’t ask if they need insurance….. They ask what gaps still exist.

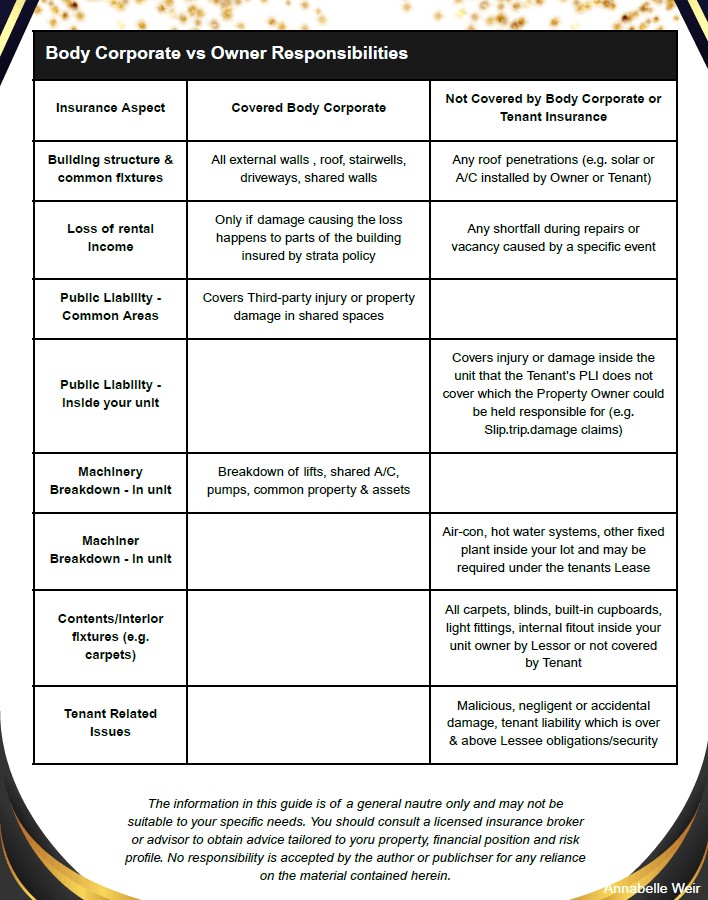

Our Head of Commercial Management has created a helpful infographic. You can also download it for future reference at a later date.

Downloadable:

Insurance Infographic: Body Corporate vs Owner Responsibilities

Disclaimer:

The information contained in this article is provided for general information purposes only and is not intended to constitute legal, financial or other professional advice. Whilst every effort has been made to ensure the content is accurate and current at the time of publication, no warranty is given as to its accuracy, completeness or suitability.

This article does not take into account your particular objectives, circumstances or needs. You should not act or refrain from acting on the basis of any content without obtaining independent, tailored advice from a qualified professional. To the maximum extent permitted by law, Ray White Commercial CSR and its officers, employees and agents disclaim all liability for any loss, damage or liability arising from reliance on, or use of, this article or its contents.